Executive Summary

- On 9 September 2024, the legislation to enact Australia’s mandatory climate-related financial disclosure regime was passed by Parliament, which will be effective for financial years beginning on or after 1 January 2025.

- The final version of the legislation is largely consistent with the version that was originally introduced to parliament in March 2024.

- The key change was the introduction of a requirement that scenario analysis disclosures will need to consider two scenarios, being a scenario where global average temperature increase is limited to no more than 1.5 degrees and a scenario where the global average temperature increase well exceeds 2 degrees.

Introduction

ESG reporting is an organisation’s public disclosure of its environmental, social, and corporate governance data, hence the ESG. The purpose of an ESG report is to ensure transparency into the organisation’s ESG activities and measure its sustainability performance so stakeholders, such as investors, consumers, and NGOs, can make better-informed decisions.

In the past years, investors’ attention to Environmental, Social, and Governance (ESG) considerations has boomed. From being seen as a niched investment just a few years ago, it is now often a deal-breaker for whether an organisation succeeds or fails.

The number of countries implementing mandatory ESG reporting is ballooning all around the world. Find out whether your organisation is affected. This article looks at recent Australian reporting requirements and covers briefly other countries that have mandatory requirements, such as New Zealand, UK, EU, USA, Canada, Malaysia and China.

Why Mandatory ESG Reporting?

The negative impact of climate change on businesses is already having visible effects in all sectors, and understanding environmental, social, and governance (ESG) risks becoming increasingly important, and more and more companies are being asked by investors to disclose their data.

The question is, should such reports be mandatory?

International Sustainability Standards Board (ISSB)

In Sept 2020, the IFRS Foundation issued a ‘Consultation Paper on Sustainability Reporting’ (IFRS, 2020) floating the idea of an International Sustainability Standards Board (ISSB) to replace a confusing mixture of disclosure practices that some companies now use to assess the impact of climate change and develop a single global disclosure standard for listed companies to report the impact of climate change on their businesses.

The basic idea behind the ISSB was to set standards for reporting on a company’s performance on material sustainability issues. The rationale for ISSB Reports was that there is a strong relationship between financial and sustainability performance; and therefore, that investors need relevant, reliable, and comparable information for both.

Many academics, and the ICMA (ANZ), pointed out that the research in this area is very conflicting and that there is a counter view that sustainability is disconnected from ‘enterprise value creation’, and ‘capital market efficiency’, and that there is no justification for making them sustainability reports mandatory.

Despite the strong views that companies do not need such an added cost, the powerful Financial Accounting lobby launched in 2021 at the United Nations Climate Change Conference in Glasgow (COP26). The rationale put by the financial accounting profession is that an internationally harmonised set of sustainability metrics and standards should: make the data on which investment decisions are made more reliable and comparable; and that this should lead to less costly due diligence, better investment pricing and ultimately stronger outcomes for investors. The consultation paper claimed that the ISSB standards will elevate sustainability reporting to the same level of rigour and acceptance as financial reporting.

Many viewed, cynically that ‘ISSB Sustainability Reports’ will be as fraught with similar valuation errors as IFRS Financial Reporting; and that he Financial Accounting profession is strongly supporting such mandatory reporting as it is another income stream for their members.

Despite such objections, the idea was accepted at COP 26. Thus, If an organisation has not been affected already, it is probably just a matter of time until it becomes mandatory for certain sized businesses to start to collect, analyse and report mandatory ESG risks.

Since COP 26, an increasing number of countries have legislated mandatory ESG regulations – and more are on the horizon. Australia is the latest country. Despite clear research evidence, the argument that the lack of availability and quality of companies’ ESG information hinders investors from making informed and sustainable investment decisions – and thus slows down the transformation to a greener economy – is now accepted by legislators.

To bridge this perceived gap between the demand for ESG information by investors and the supply of information by firms, more countries are adopting mandatory ESG disclosure legislation. A Harvard study in 2021 identified 25 countries that introduced mandates for firms to disclose ESG information during the sample period – most applying to financial institutions, state-owned companies, and large, listed companies. This does not mean that other businesses will not be affected. SMEs are already facing increased pressure from in-scope financial institutions and companies to disclose their ESG metrics (Sautner, 2021).

This article summarises the global situation, and particularly details the legislation just passed by Parliament in Australia.

Australia

The Australian Parliament has recently passed legislation to enact Australia’s mandatory climate-related financial disclosure regime.

On 9 September 2024 the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill 2024 was passed by Parliament, with Schedule 4 dedicated to Australia’s new climate-related financial disclosure regime.

The final version of the legislation is largely unchanged from the version that was originally introduced in March 2024, but there are some limited changes that entities should be aware of.

The Bill covers:

- Reporting entities: :those with Corporations Act Chapter 2M reporting obligations meeting prescribed thresholds will be required to prepare a sustainability report

- Phasing: timing of first reporting based on size or level of emissions

- Reporting content: as required by ASRS Standards (see below)

- Reporting framework: within a sustainability report in the annual report and lodged in accordance with current annual reporting requirements

- Assurance requirements: phased approach with reasonable assurance of all climate disclosures made from 1 July 2030 onwards

- Liability and enforcement: modified liability approach for both directors and auditors to disclosures of Scope 3 emissions, scenario analysis, transition plans and climate-related forward-looking statements.

Australian Sustainability Reporting Standards—Prescribed Disclosures

The first Australian Sustainability Reporting Standards (ASRS) are close to finalisation after the Australian Accounting Standards Board (AASB) discussed final working drafts at its meeting on 26 August 2024, comprising:

- AASB S1 General Requirements for Disclosure of Sustainability-related Financial Information (equivalent to IFRS S1)—available for voluntary adoption

- AASB S2 Climate-related Disclosures (equivalent to IFRS S2)—mandatory adoption.

AASB S1 and AASB S2 will be effective from 1 January 2025 and are applicable for both profit and not-for-profit entities.

AASB S1 and AASB S2 are aligned internationally to IFRS S1 and IFRS S2. The main difference to the ISSB™ Standards is that AASB S2 does not require the disclosure of industry-based metrics and reference to SASB Standards.

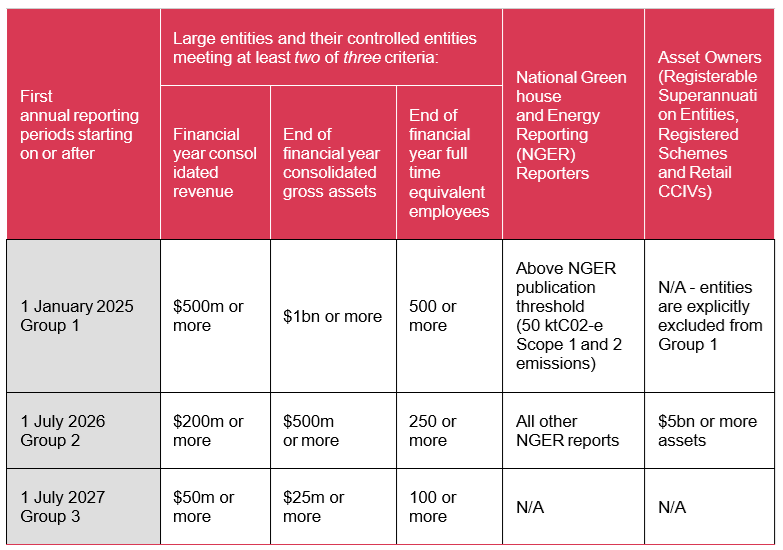

Who is required to report and when does it apply?

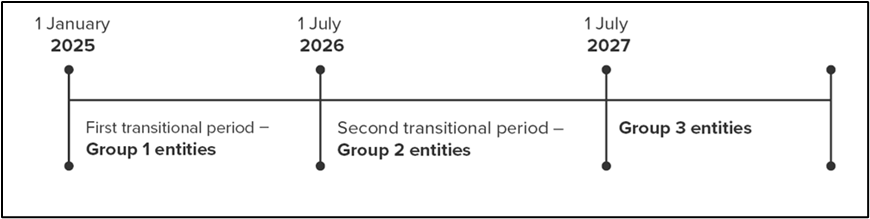

Group 1 entities must report for financial years beginning on or after 1 January 2025. Group 2 and Group 3 entities must report for financial years commencing on or after 1 July 2026 and 1 July 2027, respectively (See Table 1).

- Entities that report under Chapter 2M of the Corporations Act (including listed and unlisted companies and financial institutions, registrable superannuation entities and registered investment schemes) that meet any one of the following for a financial year are required to prepare a sustainability report in line with the timeline set out in the table below:

- Two of the three stipulated size criteria (consolidated revenue, consolidated gross assets and consolidated number of FTE employees); or

- is a registered corporation under the NGER Act (or required to make an application to register); or

- is an asset owner (defined as registrable superannuation entities, registered schemes and retail Corporate Collective Investment Vehicles (CCIVs)) where the value of assets at the end of the financial year (including the entities it controls) is equal to or greater than $5bn.

Exemptions are available for:

- Small businesses below the relevant size thresholds

- Entities exempted from lodging financial reports under Chapter 2M of the Corporations Act (for example ACNC registered Australian Charities and Not-for-profits).

Table 1: Reporting Entities and Periods

An asset owner is a registered scheme, a registrable superannuation entity or a retail corporate collective investment vehicle. An ‘asset owner’ cannot be a Group 1 entity, even if it would otherwise meet the criteria to be a Group 1 entity. An asset owner can be a Group 2 entity either by meeting the criteria applicable to all entities, or by having $5bn or more in assets.

All entities within Group 1 and Group 2 would be required to prepare a sustainability report for the year consistent with the relevant sustainability standards issued by the AASB. All entities within Group 3 are also subject to this requirement, unless the relevant entity does not have material climate risks and opportunities, whereby they are exempt from preparing a full sustainability report. Instead, these entities need to make a disclosure of a statement that they do not have material climate risks and opportunities, and the reasons why.

The Timeline of What Reporting is Required

Reporting would need to be consistent with the relevant sustainability standards issued by the AASB. The legislation enables the AASB to make enforceable sustainability standards. The AASB has previously shared the exposure draft for the Australian Sustainability Reporting Standards (ED SR1) and expects to issue final standards around Q4 2024.

Table 2: Climate Reporting Timeline

Other Countries affected by mandatory ESG reporting

Mandatory ESG reporting in New Zealand

The New Zealand government has adopted legislation making climate-related disclosure mandatory for large publicly listed companies, insurers, banks, non-bank deposit takers, and investment managers from the 2023 financial year and forward.

The legislation requires financial institutions covered by the Financial Markets Conduct Act to report, these are:

- Registered banks, credit unions, and building societies with total assets of more than 1 billion NZD.

- Managers of registered investment schemes with greater than 1 billion NZD in total assets under management.

- Licenced insurers with greater than 1 billion NZD in total assets or annual premium income greater than $250 million.

Mandatory ESG reporting in the UK

In April 2022, the UK enacted two mandatory ESG disclosure laws. These are:

These Regulations require certain companies to provide climate-related financial disclosures in their strategic report. These companies are:

- All UK companies that are currently required to produce a non-financial information statement, being UK companies that have more than 500 employees and have either transferrable securities admitted to trading on a UK regulated market or are banking companies or insurance companies (Relevant Public Interest Entities (PIEs));

- UK registered companies with securities admitted to AIM with more than 500 employees;

- UK registered companies not included in the categories above, which have more than 500 employees and a turnover of more than £500m;

- Large LLPs, which are not traded or banking LLPs, and have more than 500 employees and a turnover of more than £500m and;

- Traded or banking LLPs which have more than 500 employees.

The impact of the new legislation will not only be on the UK’s largest companies and financial institutions but also on the thousands of businesses in their supply chains—stressing once again the importance of getting your ESG reporting going despite of whether you are directly affected or not.

Mandatory ESG reporting in the EU

Prior, certain large companies (around 11.000 entities) within the EU were required to disclose ESG information under the Non-Financial Reporting Directive (NFRD).

However, in 2023, the NFDR was replaced by a new ESG reporting directive—the Corporate Sustainability Reporting Directive (CSRD). The CSRD will significantly extend the scope of companies obliged to comply with approximately 50.000 companies in the EU, corresponding to 75% of the EU’s companies’ turnover.

Mandatory ESG reporting in the US

There are currently no mandatory ESG disclosure requirements on the federal level in the US. However, in May 2022, the US Securities and Exchange Commission (SEC) proposed “amendments to rules and reporting forms to promote consistent, comparable, and reliable information for investors concerning funds’ and advisers’ incorporation of environmental, social, and governance (ESG) factors.” If the proposal is adopted, it will establish disclosure requirements for funds and advisers that market themselves as having an ESG focus and be a large win against ESG greenwashing.

Mandatory ESG reporting in Canada

In April 2022, the Canadian federal government released its 2022 budget, where they promised to bring mandatory climate-related reporting requirements to federally regulated banks and insurance companies. The financial institutions in scope will be required to publish their climate disclosures in alignment with the TCFD framework, starting in 2024.

Although the regulation focuses on federally regulated financial institutions, the government expects it to have an impact on Canada’s entire economy. The budget document reads:

“As federally regulated banks and insurers play a prominent role in shaping Canada’s economy, OSFI guidance will have a significant impact on how Canadian businesses manage and report on climate-related risks and exposures.”

Mandatory ESG reporting in Asia

Malaysia: In Malaysia, ESG reporting has been mandatory for all publicly listed companies since 2016, making it one of the first countries to introduce this kind of disclosure requirement. Today, there is no consistent ESG reporting framework mandated. Still, a proposal issued in March 2022 suggests that all in-scope companies should disclose the information aligned with the TCFD recommendations—an update that is probably two or three years down the road.

China: There is currently no mandatory ESG reporting legislation in China. However, with effect from 1 June 2022, China’s first set of (voluntary) guidelines for Chinese companies to report on ESG metrics came into effect— the Guidance for Enterprise ESG Disclosure. It was developed by the Beijing-based think tank China Enterprise Reform and Development Society, focusing on Chinese companies, laws, regulations, and policies. While it is non-binding, the framework offers “a glimpse of what mandatory disclosures might eventually look like in the country,” according to Bloomberg.

Summary

Despite the lack of strong research evidence that there was any relationship between financial and sustainability performance, the ISSB was launched in 2020 to issue standards for reporting on a company’s performance on material sustainability issues.

Since then, an increasing number of countries have legislated mandatory ESG regulations – and more are on the horizon. Australia is the latest country.

This article looks at recent mandatory reporting requirements in Australia; and also covers briefly other countries that have mandatory requirements, such as New Zealand, UK, EU, USA, Canada, Malaysia and China.

References

IFRS® Foundation (2020), Consultation Paper on Sustainability Reporting, September, pp. 1-20.

Sautner, Zacharias (2021) “The Effects of Mandatory ESG Disclosure around the World”, Harvard Law School Forum on Corporate Governance, May 10, p.1. https:// corpgov.law.harvard.edu/2021/05/10/the-effects-of-mandatory-esg-disclosure-around-the-world/