Introduction

The ‘Earth system’ is the culmination of all of the physical, chemical, and biological activities that occur on the planet. According to the principles of physics and biochemistry, the Earth system is made up of numerous interrelated processes (including transpiration, photosynthesis, and evaporation) that store, transport, and change matter and energy (Skinner, 2011).

The Earth system can function in a certain steady state for many thousands of years when its processes are in harmony. However, major disturbances to Earth-system processes can lead to an abrupt change of state.

Certain outside variables, like the sun’s output or the geometry of Earth’s orbit around it, have the power to alter the planet’s state and are obviously not under human control. On the other hand, scientists believe that it is human activity over the next 50–100 years that will most likely determine the state of the planet. Human activity is the only factor affecting the state of the planet that is within our control.

Planetary Boundaries (PBs)

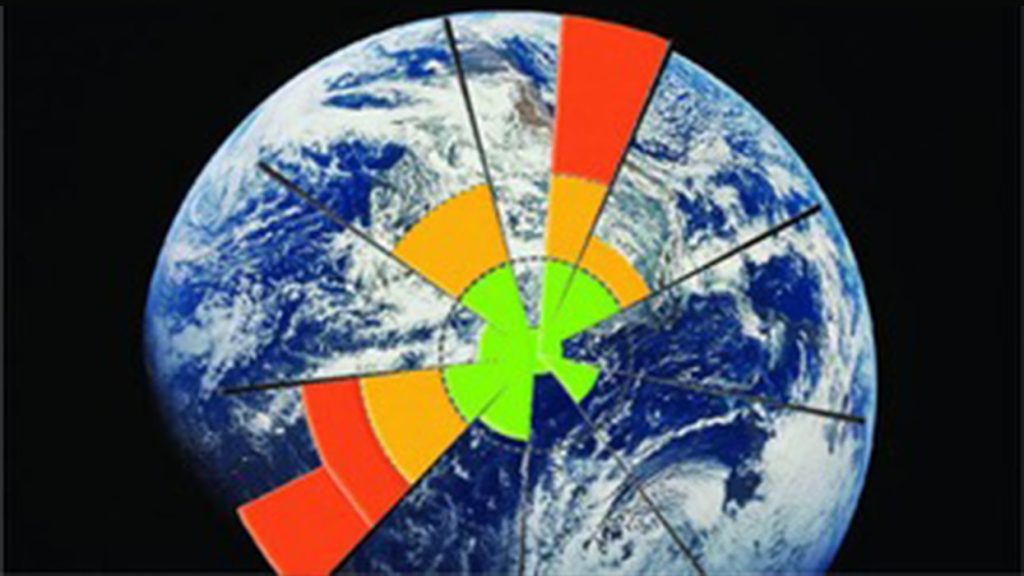

Nine Planetary Boundaries (PBs), or the limits for Earth-system processes within which there is little chance of a departure from the current state, were postulated by Rockström et al. (2009) (see Table 1). These Boundaries collectively establish a “safe-operating-space” for people.

Unfortunately, six of the planetary boundaries— novel entities, climate change, biosphere integrity, land-system change, freshwater change and biogeochemical flows—have already been crossed. According to Steffen et al. (2015), all of them are dependent on the condition of the Earth’s soil. Soil condition refers to the state of the soil, which includes its physical, chemical, and biological characteristics and the processes and interactions that connect them; and which in turn determine the capacity of the soil to support ecosystem services.

The Planetary Boundaries indicate that we are now residing outside of the safe operating space, giving us an idea of the severity and urgency of the crisis. The issue is, can we, as management accountants, contribute to fix this planetary problem?

| Earth system process | Control variable | Planetary Boundary |

| Climate change | Atmospheric concentration of carbon dioxide | ≤ 350 ppm |

| Change in radiative forcing | ≤ 1 W/m2 | |

| Biodiversity loss | Global extinction rate | ≤ 10E/MSY |

| Biogeochemical flows (Nitrogen and phosphorus cycles) | Reactive nitrogen removed from the atmosphere | ≤ 62Tg |

| Phosphorous flowing into oceans | ≤ 11Tg | |

| Land-system change | Area of forested land as a percentage of original forest cover | ≥ 75% |

| Stratospheric ozone depletion | Stratospheric concentration of ozone measured in Dobson Units (DU) | ≤ 5% below pre-industrial levels (290 DU) |

| Ocean acidification | Mean saturation state with respect to aragonite in the oceans | ≥80% of the pre-industrial level |

| Fresh water use | Freshwater consumption | ≤4000 km3/yr |

| Novel entities | NA | NA |

| Atmospheric aerosol loading | Aerosol optical depth | NA |

| Regional limit of ≤0.25 | ||

| Table 1 Summary of the Planetary Boundaries (adapted from Steffen et al., 2015) | ||

Clearly, management accountants are not trained to comprehend or analyse the information on planetary boundaries given in Table 1, let alone formulate strategies to mitigate the consequences of exceeding these PBs. However, management accountants are very concerned in the allocation of scarce resources in meeting the twin challenges of sustaining lives and livelihoods, and the accountability issues that surface in crisis scenarios.

Therefore, the allocation of societal responsibilities to ensure humanity stays within its planetary boundaries requires the formation of social purpose alliances with multiple disciplines. It is by leveraging the strengths of multiple disciplines that humanity can respond to crises such as global pandemics and climate challenges. In situations of scarce resources, management accountants play a crucial role in providing data-driven insights and cross-functional knowledge to inform strategic planning across a range of domains, such as climate risk mitigation, carbon emissions reduction goals and equitable allocation of resources.

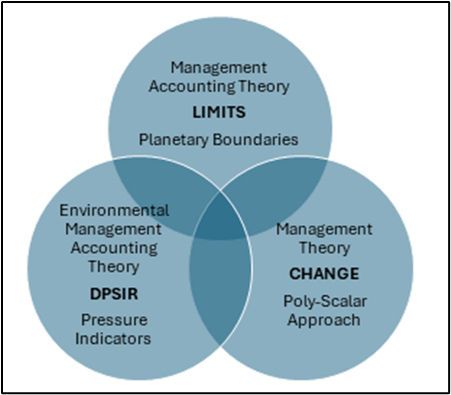

This article provides an overview of a novel paradigm for regulating planetary boundaries that combines theories from three branches of knowledge as first postulated by Meyer & Newman (2018) and requires a multidisciplinary approach. These are:

- Management theory shows that the most effective approach to managing the Earth system is likely to be a poly-scalar approach, i.e., one that can be applied in different ways, across different areas of society, and at different scales, which is coordinated by a general system of rules. A poly-scalar approach does not rely on a global approach. Efforts at different scales can thus begin right away. This does not preclude the continued efforts to agree to top-down solutions—which will almost certainly play a critical element in successful management of the Earth system (e.g. the Paris Accord).

- Management accounting theory which highlights the importance of measuring and monitoring the allocation of resources and the performance of assets and flows in order to make informed decisions.

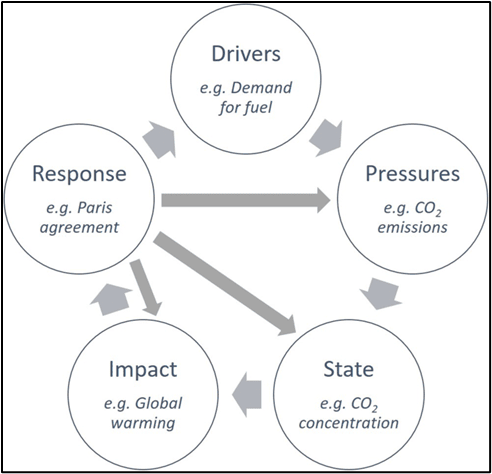

- Environmental management accounting theory which demonstrates that the type of indicator selected is critical to the applicability to policy and behaviour applications; in this case, it highlights the need to convert the PBs into pressures on the environment. It uses a DPSIR (Drivers, Pressures, States, Impacts, Responses) framework to look at and analyse the important and interlinked relationships.

The purpose of this article is to summarise the work of Meyer & Newman (2018), who suggested a new paradigm called the Planetary Accounting Framework (PAF) and make it applicable to management accountants via a Planetary Management Accounting Framework (PMAF). The PMAF is based on the allocation of Planetary Quotas and Planetary Boundaries. The Planetary Quotas are limits for human activities which are derived from the Planetary Boundaries. They show what is needed to return to and live within a safe operating space.

The domains of the three aforementioned theories Limits (Planetary Boundaries), Change (poly-scalar management) and Pressures (environmental management accounting), overlap to create the novel concept of the Planetary Quotas (Figure. 1). As a result, these adhere to the Sustainable Earth philosophy, which links science and the Planetary Boundaries to community and corporate policy.

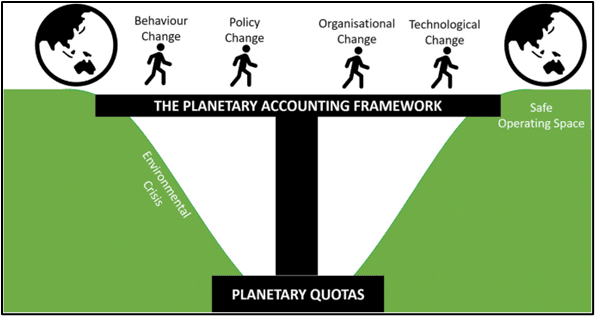

As shown in Figure. 2, this framework provides the platform for behavioural, policy, technological, and organisational change.

The Theoretical Foundations for an Integrated Approach

This section presents an overview of the theories from the three branches of knowledge described above, which together provide an integrated approach to change with respect to the Planetary Boundaries. It is shown how the Planetary Quotas can be derived from the Planetary Boundaries.

Poly-Scalar Management: A Strategy to Regulate the Earth System.

Taking care of the Earth system is not an easy undertaking. The majority of theories from the past on the best ways to manage shared resources (such fisheries, forests, or the atmosphere) concluded that the only viable options were private management or top-down governance (Meyer & Newman, 2018). The underlying presumptions of these ideas, which relied on basic game theory, were that individuals will always act to maximise their own gain regardless of the greater good. According to Hardin (1968), the “tragedy of the commons” is that human nature will force people to keep using resources excessively for short-term, selfish gain until everyone suffers.

However, these ideas fall short of explaining how communities function in real life and how social science has come to grasp how human behaviour can collectively bring about change. Communities and cultures are created to facilitate the pursuit of more general objectives than just selfish gain. The question then is, if top-down governance and private action do not address our understanding of social science and change, what sort of global environmental management structures would be more effective?

Managing human behaviour entails managing human impacts on the environment. This could refer to an individual’s daily conduct, the choices made by a CEO, a public servant, or a community member. Research grounded on observed behaviour reveals that a wide range of factors impact decisions, and that behaviour is very unpredictable. A person’s lifestyle, social standing in the family, the workplace, motivations, past actions, habits, societal conventions, context, and technology all come into play. Historically, attempts to modify behaviour have generally focused on social conventions, as well as personal and communal values. The results, which show that context and technology play major roles in shaping decision-making, emphasise the significance of infrastructure, technology, and therefore governance and industry in influencing decisions that are pro-environmental or otherwise. For example, social media has been observed to unintentionally encourage younger generations to transition from private to public transportation since it enables them to maintain social connections with their peers while commuting.

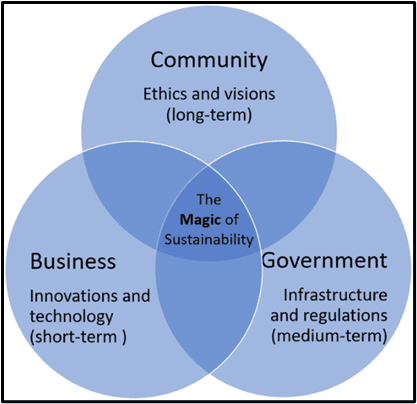

The findings corroborated by the science of change indicate the importance of various activity scales. It shows that infrastructure and technology, in addition to one’s community, are crucial for bringing about change. The notion that integrated community, corporate, and governmental solutions can significantly outperform the sum of their parts is known as the “magic of sustainability” (Figure 3). More specifically, extremely creative and effective solutions that support change can arise when long-term community values and ethics coincide with mid-term government rules and infrastructure as well as short-term business advances.

Drawing from these theories, Meyer & Newman (2018) proposed that the most effective approach to change is likely to be one that is:

“…integrative across different scales, sectors, and timeframes, that is not controlled by a single body, but which could be implemented through government, private action, or self-organised management, that is coordinated by a general system of rules which have different mechanisms at different centres of activity.”

Benefits of such an approach to managing the Earth system include:

- the possibility for immediate action at different scales—rather than a need to wait for global accord,

- the facilitation of widespread experimentation and learning at multiple scales—rather than the need to determine an effective approach prior to rolling out global initiatives,

- the flexibility to encompass different centres of decision-making which are formally separate —creating a bridge that is necessary to achieve change, and most of all

- the ability to engage people in whatever scale of activity they can focus on.

The Application of Management Accounting Theory to Establish a Common Empirical Foundation for Various Environmental Challenges

Management accounting theory highlights the importance of measuring and monitoring the performance of assets and the resultant flows in order to make informed decisions. Management accounting focuses on preparing statements, reports, and documents that help management in making better decisions related to their business’ performance. Management accounting today has wide applicability, from strategic cost management to strategic business analysis encompassing areas of environment, society and governance (ESG).

Environmental management accounting (EMA) can be defined as the identification, collection, estimation, analysis, internal reporting, and use of materials and energy flow information, environmental cost. information, and other cost information for both conventional and environmental.

Environmental Impact Assessment (EIA) is the quantification of environmental damage from human activity. Environmental management accounting is the measurement and monitoring of environmental impacts over time, often against targets that can be standards or limits required to be met. EIA is a critical element in managing the impacts of human activity on the environment. It is now possible to estimate the environmental impacts of not only past and present but also future activities with increasing levels of accuracy. Thus, decision making, planning, policy, and legislation can all be made with some understanding of the corresponding environmental implications. For this reason, EIA is common practice for many businesses, cities, and nations and can also be undertaken to evaluate the impact of individuals, groups of people, or products and services.

Environmental limits or standards are not new; for example, the use of environmental footprints and/or life cycle assessments to help manage the global environment is commonplace. An example is the Ecological Footprint, a measure of human use of natural capital compared to the corresponding biological capacity—or available natural capital. This framework is used to assess the impacts of most nations and has been used in other smaller-scale applications, such as the development of an online personal impact calculator.

The primary shortcoming of using environmental footprints, footprint families, and EIA in general to manage impacts is that the results are rarely given in the context of science-based targets. Targets are often self-selected. They are typically based on a percentage improvement from a previous reporting period, sectoral commitments (for example, national commitments to meet carbon targets), or using sectoral or industrial benchmarks.

Carbon Emissions and Sequestration (CES) accounting is a strand of environmental management accounting where global limits are often considered. There are debates as to a “safe” level of global warming and therefore the maximum allowable CO2 emissions. Nonetheless, it is possible to link CO2 emissions for an activity with a global budget based on scientific knowledge (Ratnatunga, et. al., 2011).

CES accounting has led to a widespread understanding of what is a relatively complicated scientific problem. It is used across different sectors and at different scales of activity. Individuals and communities can calculate their “carbon footprint”—the amount of CO2 released due to the activities of the individual or community. Formal greenhouse gas accounting protocols have been developed for nations, cities, and products and services. CO2 emissions have been translated into dollar values. Studies have been completed to assess the relative benefits of a carbon tax versus carbon trading. Different approaches for managing emissions and different technologies for reducing emissions or absorbing carbon from the atmosphere have been trialled in different locations and at different scales, allowing for a very rapid uptake of knowledge and development.

CES accounting is a remarkable example of the importance of limits. These efforts at every scale have already led to some success. For example, ‘Net-Zero’ is a target of completely negating the amount of greenhouse gases produced by human activity—to be achieved by reducing emissions and implementing methods of absorbing carbon dioxide from the atmosphere.

In summary, to better manage the global environment, the results of environmental impact assessments should be compared to absolute limits rather than incremental targets. We can use such an approach to drive systemic change. The PBs are absolute global limits. However, they cannot easily be connected to environmental impact assessments.

The DPSIR Accounting Framework and Obtainable Indicators for Environmental Management Accounting.

The DPSIR (Drivers, Pressures, States, Impacts, and Responses) framework is employed to examine and evaluate the significant and interconnected connections. The PBs have already been used in a number of attempts, at various scales, for accounting in environmental management. There have been multiple endeavours to establish a connection between the PBs and the current environmental assessment frameworks, such as life-cycle evaluations and footprint tools. Based on the PBs, regional and national targets have been created, and EMA reports have been published using these targets.

Nevertheless, the work is fragmented and lacks a holistic focus because the planetary scientists who first proposed the PBs did not intend for them to be disaggregated or scaled. The purpose of the PBs was to provide a clear snapshot of the status quo of critical Earth-system processes based on how these systems are measured globally. They were not meant to define limits for human activity.

There are serious restrictions on all of the works that scale or alter the PBs and use them for EMA targets. For example, none of them correspond to the PB for climate change. There is a wide variation in the indicators selected for biosphere integrity. So much so that it would be very difficult to contrast and compare any of the limits with one another or with the original PB. The markers chosen to measure the integrity of the ecosystem differ greatly. It would be exceedingly challenging to contrast and evaluate any of the restrictions with the original PB or with one another because of this. Perhaps more crucially, none of the adaptations work well outside of the original context in which they were designed. It would be challenging to apply the produced national indicators to the local or regional levels or to convert them into corporate objectives. This implies that even within that nation, different levels of activity would be working towards different targets. The level of effort that has gone into each of the adaptations is high. It would not be practical to repeat such an involved process for every intended use.

Whilst boundaries cannot easily be scaled or used in EMA, the DPSIR framework enables a more precise classification and, therefore, a better understanding of indicators. As such, it can be used to translate indicators from one category to another, as there is a causal relationship between each category.

- Driver indicators describe human needs. Some examples of Driver indicators include kilowatt hours of electricity, kilometres travelled, or litres of fuel for transport.

- Pressures which result from drivers that flow to the environment. One Pressure indicator resulting from the Driver indicators listed is CO2

- State indicators describe the environment. State indicators provide a snapshot of the status quo. Comparing the current State of a given ecosystem to a previous State allows us to understand the influence of human activity on the environment. For example, the change of the State indicator which corresponds to CO2 emissions—the concentration of CO2 in the atmosphere—has allowed us to understand the ramifications of emitting CO2. It is this sort of indicator that is commonly used in State of the Environment Reporting.

- Impact indicators describe the results of changing environmental States. For example, one of the Impacts of the increased concentration of CO2 in the atmosphere is an increase in average global temperature. Another Impact is species extinctions.

- Response is not a category of indicator. Rather, it is included in the framework to show that different types of responses can be linked to different categories of indicators (see Figure 4)

Human activity directly influences Pressures and Drivers and only indirectly influences States and Impacts. As a result, State and Impact indicators are helpful for characterising the current situation and tracking changes over time.

There is no straightforward way to divide the responsibility for the concentration of CO2 in the atmosphere between different nations, cities, regions, or individuals unless a different indicator can be found that is easily scaled. Nor can one directly compare specific human activities to the global average temperature. An individual deciding whether to take the car or train to work, or a local government deciding whether to proceed with certain infrastructure—neither could begin to estimate the impacts of these decisions on the atmospheric concentration of CO2. It is only when these indicators are translated to a Pressure indicator (e.g. CO2 emissions) that it becomes possible to begin to allocate this global budget between nations, cities, or any other level.

These indicators are, nevertheless, difficult to connect to human activities. Until a suitable, easily scalable indicator is discovered, there is no simple method to determine the responsibility for the concentration of CO2 in the atmosphere to different countries, cities, regions, or individuals. Neither can particular human actions be directly compared to the average global temperature. A person choosing to drive or use public transportation to work, or a local government choosing to move forward with a certain piece of infrastructure, could not begin to calculate the effects of these choices on the amount of CO2 in the atmosphere. It is only when these indicators are translated to the Pressure indicator – CO2 emissions, that it becomes possible to begin to allocate this global budget between nations, cities, or any other level.

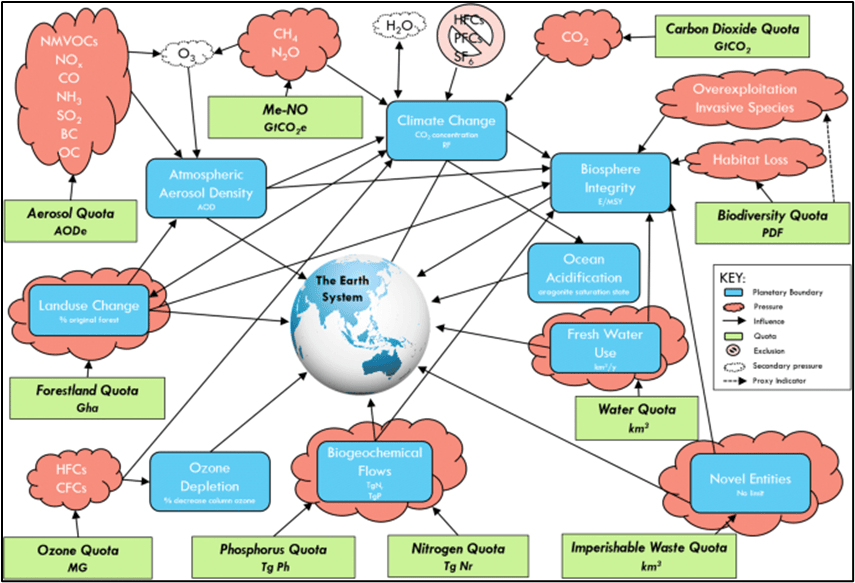

Developing the Planetary Quotas

The Planetary Boundaries are presented as distinct control variables with explicit limits. This is by design to make them easily communicable. In practice, there is a high level of interconnectivity between the PBs. For example, almost every PB affects biosphere integrity. Exceeding one PB affects our ability to remain within others.

This interconnectedness of PBs needs to extend to the Planetary Quotas (PQs) in order for them to be a reliable translation of the PBs. Translating each PB into a PQ without taking into account the other PBs and PQs would not be appropriate.

There are many pressures that only have minor contributions towards the PBs; therefore, Meyer & Newman (2018) applied an exclusion protocol for pressures that contributed less than 1% towards current global impacts. Excluding minor impacts is common practice in environmental assessment protocols as a means to simplify the process with minimal effect on the results. In total, thirty-two critical pressures were found. These were then analysed to determine which of the pressures could be grouped, and to find appropriate Pressure indicators to assess them with. The result was ten Pressure indicators, which formed the basis of the PQ development.

Each of the PQ indicators found corresponds to one or more of the critical pressures and, therefore, one or more PB(s). The PQ limits were thus determined by assessing each of the corresponding PBs and selecting the most stringent limit.

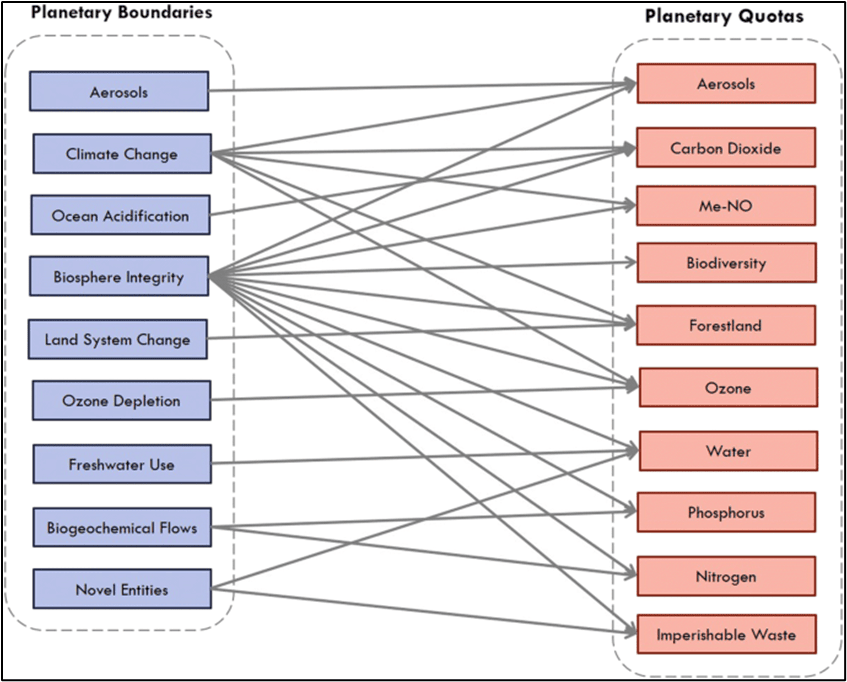

Figure 5 illustrates how the PBs are translated to pressures and then to PQs. Figure 6 illustrates the direct relationship between the PBs and PQs. Two of the Planetary Boundaries have previously been identified as “core boundaries” for their high level of interconnectivity: Climate Change and Biosphere Integrity. Each of these correspond to more than half of the Planetary Quotas (see Figure 6).

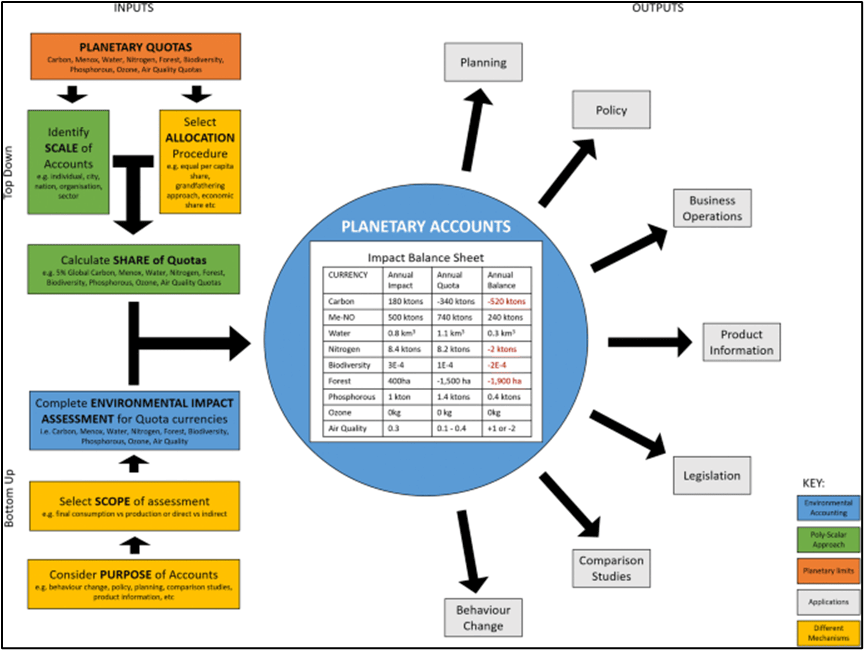

The Planetary Management Accounting Framework

The Planetary Quotas form the foundations for the new Planetary Management Accounting Framework (PMAF). The PMAF shows how the PQs can be used in a poly-scalar approach to manage global impacts. It can be used to assess the impacts of different scales of human activity against planetary limits. Figure 7 shows how the Framework can work for different scales and purposes.

The left-hand side shows the inputs, and the right-hand side shows the outputs. The inputs are both top-down (scaling the Planetary Quotas to the scale of assessment) and bottom up (using environmental impact assessment methods to estimate impacts in each environmental activity).

Summary

Planetary Management Accounting is a novel framework that could facilitate an unprecedented, global, multi-scaled approach to managing the Earth system. Environmental management accounting has advanced to the point that we can estimate what the environmental impacts of an activity are or will be. Three theories: (1) Management theory; (2) Management Accounting theory; and (3) Environmental management accounting theory have been advanced in the literature, but they have been disconnected from one another. The Planetary Management Accounting Framework, based on the new Planetary Quotas, brings these three theories together.

References

Hardin G. (1968), “The tragedy of the commons”. Science. 162:1243–8.

Meyer. K. & Newman, P. (2018), “The Planetary Accounting Framework: a novel, quota-based approach to understanding the impacts of any scale of human activity in the context of the Planetary Boundaries”, Sustainable Earth, 25 October, 1(4), https://sustainableearthreviews.biomedcentral.com/articles/10.1186/s42055-018-0004-3#

Newman P. (2005) “Can the magic of sustainability revive environmental professionalism?” Greener Management International, 49:11–23.

Ratnatunga, J., Jones, S., and Balachandran, K.R (2011) “The Valuation and Reporting of Organizational Capability in Carbon Emissions Management”, Accounting Horizons, 25(1): 127-147.

Rockström J., et al. (2009), “Planetary boundaries: exploring the safe operating space for humanity”. Ecology and Society, 14, 32.14:32.

Skinner B.J. (2011), “The blue planet: an introduction to earth system science / Brian J. Skinner, Barbara Murck. 3rd ed. Hoboken: Wiley.

Steffen W. et.al., (2015), “Planetary boundaries: guiding human development on a changing planet”. Science. 347:1259855.