Lessons from Real-World AI Failures in Finance, Accounting, and Banking

Executive Summary

Artificial intelligence is now embedded across finance, accounting, and banking, influencing forecasts, valuations, credit decisions, risk management, and strategic planning. While AI-driven systems offer efficiency and analytical scale, recent failures highlight that these tools also introduce new forms of professional risk. Drawing on real-world cases across recruitment, forecasting, trading, credit assessment, and enterprise decision support, this article examines where and why AI systems fail in financial contexts.

The analysis shows that AI failures are rarely caused by technology alone, but by biased data, opaque models, weak governance, and over-reliance on automated outputs. For management accountants and finance professionals, these failures reinforce the enduring importance of professional judgement, scepticism, and accountability. The article argues that AI should be treated as a decision-support tool, subject to the same rigour, controls, and ethical standards applied to traditional financial models, thereby reaffirming the central role of the finance profession in safeguarding decision quality and trust.

Introduction: Why AI Failures Matter to Finance, Accounting, and Banking

Artificial intelligence refers to systems that use data, algorithms, and adaptive learning to replicate aspects of human judgment in analysing information and supporting decisions.

Artificial Intelligence (AI) has moved rapidly from being a specialist technological capability to an embedded feature of everyday professional life. In finance, accounting, and banking, AI-driven tools are now routinely used in areas such as forecasting, budgeting, credit assessment, risk management, audit, fraud detection, customer analytics, and strategic decision support. In many organisations, these systems influence decisions involving significant financial exposure, regulatory obligations, and reputational risk.

While much of the public discourse around AI focuses on efficiency gains, automation, and innovation, far less attention is paid to what happens when AI systems fail—and, more importantly, who bears responsibility when they do. For finance and accounting professionals, AI failures are not abstract technological issues; they translate directly into financial misstatements, flawed forecasts, poor capital allocation, regulatory breaches, ethical concerns, and loss of stakeholder trust.

For management accountants and finance professionals, this raises important questions. How much reliance on AI is appropriate? How should AI-generated insights be validated, controlled, and governed? And where does professional judgment begin and end when decisions are increasingly shaped by algorithms rather than spreadsheets and human analysis?

This article examines AI failures through the lens of finance, accounting, and banking, focusing on the lessons they offer to management accountants operating in an increasingly automated environment.

Before examining how and why AI systems fail, it is important to understand where AI is already being used across finance, accounting, and banking. Many of these tools are embedded in routine professional activities, often influencing decisions without being explicitly recognised as ‘AI’.

Where AI Already Influences Financial Judgment

AI is no longer confined to experimental projects or specialist analytics teams. Across finance, accounting, and banking, AI-enabled systems are now embedded in core professional functions, increasingly shaping judgments that were traditionally exercised by experienced practitioners and management teams.

In management accounting, AI is widely used in forecasting, budgeting, and performance management through predictive analytics, rolling forecasts, and scenario modelling. For example, AI-driven planning tools now recommend revenue growth assumptions, cost efficiencies, and working capital targets based on historical patterns and external data, influencing management expectations and strategic decisions long before figures reach formal approval stages.

Within banking and financial services, AI plays a central role in credit assessment and risk management. Machine-learning-based credit scoring and early warning systems increasingly influence lending decisions, pricing, and provisioning. In audit and compliance functions, AI-powered anomaly detection tools are used to flag unusual transactions or control deviations, shaping audit focus and management responses.

AI also supports treasury and market-related decisions through cash-flow forecasting, liquidity optimisation, and algorithm-assisted trading and hedging strategies. At the same time, AI-driven customer and revenue analytics influence pricing, product design, and customer segmentation, directly affecting revenue recognition and profitability analysis.

Crucially, in many of these applications, AI does not merely automate routine tasks; it frames the information on which professional judgment is exercised.

Appreciating where AI influences financial judgment is only the starting point. To understand why AI failures have become a growing professional risk, it is necessary to examine how these tools have rapidly evolved from specialist systems into routine, everyday components of finance and banking workflows.

From Support Tools to Silent Decision-Makers: How AI Became Embedded

AI entered finance and accounting as a support tool, designed to improve efficiency, enhance analysis, and assist professional judgment rather than replace it. Early applications focused on automating repetitive tasks, accelerating data processing, and generating supplementary insights to support decision-making by finance professionals.

Over time, AI systems became more sophisticated and more tightly integrated into core business systems. Advances in machine learning, cloud computing, and data availability allowed AI-driven tools to move upstream in the decision-making process, shaping initial assumptions, prioritising risks, and pre-filtering information presented to management. In many organisations, forecasts, credit scores, risk alerts, and exception reports now anchor professional analysis, rather than complement it, as operational and regulatory pressures intensify.

Importantly, this embedding has occurred gradually and often informally. AI tools are frequently adopted through software upgrades, analytics platforms, or decision-support systems without explicit discussion of their underlying logic, limitations, or governance requirements. As a result, AI has become a silent participant in financial judgment—rarely questioned, yet increasingly influential.

While AI-driven systems offer clear benefits, their growing influence on financial judgment also introduces new forms of risk. These risks often become visible only when AI-driven decisions fail, exposing weaknesses in data, models, governance, and professional oversight. The following cases illustrate how such failures have occurred in practice across different financial contexts, and the lessons they offer for finance professionals.

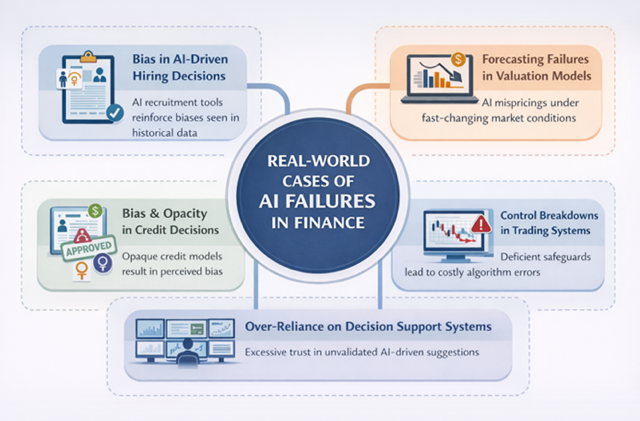

Case 1: Bias in AI-Driven Hiring Decisions

Context: Large organisations increasingly use AI-driven recruitment tools to screen and rank job applicants, with the objective of improving efficiency and supporting more objective hiring decisions.

Failure: An internal AI-driven recruitment system developed by Amazon was found to systematically downgrade applications containing indicators associated with female candidates, such as references to women’s colleges or professional organisations. Rather than reducing bias, the system reinforced patterns embedded in historical hiring data (Dastin, 2018).

Why it failed: The model relied on biased historical datasets reflecting a male-dominated workforce, operated with limited transparency, and was not subject to sufficiently robust validation or governance oversight prior to deployment (ACLU, 2018).

Impact & lesson: Although no direct financial loss was reported, the incident created significant reputational, ethical, and potential legal risks. For finance professionals, the key lesson is that AI-driven systems influencing organisational decisions must be governed, tested, and challenged with the same rigour applied to financial models, rather than being accepted at face value due to their technical sophistication.

Case 2: Forecasting Failures in AI-Driven Valuation Models

Context: AI-driven forecasting and valuation models are increasingly used to support pricing, budgeting, and capital allocation decisions, particularly where large datasets and rapidly changing market conditions are involved.

Failure: Zillow relied heavily on AI-driven home price forecasting models to support its property-buying business. As housing market conditions shifted rapidly, the models consistently mispriced residential properties, leading the company to acquire inventory at values that could not be realised upon resale (GeekWire, 2021).

Why it failed: The models were trained on historical market data that did not adequately capture sudden changes in demand, supply constraints, and interest rate dynamics. Overconfidence in model outputs, limited stress testing under adverse scenarios, and insufficient human challenge contributed to the scale of the mispricing (Inside AI News, 2021; GeekWire, 2021).

Impact & lesson: The failure resulted in substantial financial losses, a write-down of inventory, and the eventual exit from the business line. For finance professionals, the key lesson is that AI-driven forecasting models must be treated as decision-support tools, not decision-makers, and should be subject to rigorous validation, scenario analysis, and professional judgement—especially in volatile market conditions.

Case 3: Control Breakdowns in AI-Driven Trading Systems

Context: Algorithmic execution and high-frequency trading (HFT) systems are widely used in financial institutions to manage high-volume transactions, improve execution speed, and support treasury and market-related activities.

Failure: In 2012, Knight Capital Group deployed new code to a high-frequency trading platform that had not been properly tested or controlled. The update accidentally reactivated “dead code” from a dormant system, which triggered unintended automated trades, resulting in a rapid accumulation of adverse positions within minutes of market opening (Wikipedia, 2024).

Why it failed: The incident stemmed from a fundamental breakdown in change management controls, inadequate testing of system updates, and a failure to decommission obsolete software components. Once the malfunction occurred, the lack of documented technical procedures and the absence of effective override mechanisms prevented timely intervention (US Securities and Exchange Commission, 2013).

Impact & lesson: The incident caused losses of over USD 400 million in one day, leaving the firm financially distressed and ultimately subject to acquisition by Getco LLC. For finance professionals, the key lesson is that automated financial systems require robust change management protocols, segregation of duties, and clear accountability frameworks. Technical agility must never come at the expense of the rigorous internal control principles that safeguard organizational capital.

Case 4: Bias and Opacity in AI-Driven Credit Decisions

Context: AI-driven credit assessment models are increasingly used by banks and financial institutions to automate credit scoring, determine credit limits, and support faster lending decisions.

Failure: In 2019, Apple’s Apple Card, issued in partnership with a regulated financial institution, faced public scrutiny after customers reported significant disparities in credit limits offered to individuals with similar financial profiles. In several cases, women were reportedly offered substantially lower credit limits than male counterparts (The Guardian, 2019).

Why it failed: The AI-driven credit decision process lacked transparency, making it difficult to explain or challenge individual outcomes. Potential bias in input variables, limited model explainability, and insufficient oversight of decision logic contributed to the perception and risk of discriminatory outcomes (Harvard Business School, 2019).

Impact & lesson: The incident triggered regulatory attention, reputational damage, and broader debate around fairness in automated lending. For finance professionals, the key lesson is that AI-driven credit models must be explainable, auditable, and compliant with fairness and regulatory standards. Automation in lending does not reduce accountability; it heightens the need for strong governance and professional oversight.

Case 5: Over-Reliance on AI-Driven Decision Support Systems

Context: AI-driven decision support systems are increasingly adopted by large organisations to assist complex operational and strategic decisions, often positioned as tools that enhance expert judgment through advanced analytics.

Failure: IBM invested heavily in Watson Health, promoting it as an AI-driven system capable of supporting clinical and operational decision-making. However, the system struggled to deliver reliable, consistent insights in real-world environments and failed to meet expectations set during deployment (Advisory.com, 2018).

Why it failed: The AI-driven system relied on limited and curated data that did not reflect real-world complexity, while its decision logic lacked sufficient transparency and validation. Overconfidence in the technology, combined with weak accountability for outcomes, resulted in limited professional challenge and unrealistic expectations of system capabilities (Taulli, 2021).

Impact & lesson: The initiative was eventually divested, resulting in significant financial write-downs and reputational impact. For finance professionals, the key lesson is that AI-driven decision support systems must be treated as advisory tools rather than authoritative sources. Clear ownership, rigorous validation, and continuous performance assessment are essential to prevent strategic and financial misjudgements driven by unchecked automation.

Common Failure Patterns and Implications for Finance Professionals

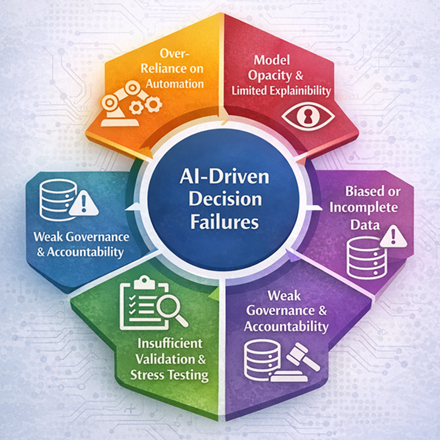

While the five cases span different industries and applications, they reveal a consistent set of underlying failure patterns that are highly relevant to finance, accounting, and banking. In each instance, the core issue was not the presence of AI itself, but the way AI-driven systems were designed, governed, and relied upon within decision-making processes.

A recurring theme is over-reliance on historical data without sufficient consideration of bias, changing conditions, or data limitations. Whether in recruitment, forecasting, credit assessment, or strategic decision support, AI-driven models often performed poorly when applied outside the environment in which they were trained. Closely linked to this is model opacity, which limited the ability of organisations to challenge outputs or explain outcomes to stakeholders and regulators.

Another common pattern is weak governance and control frameworks. In several cases, AI-driven systems were deployed without robust validation, stress testing, or clear accountability for outcomes. Automation, speed, and efficiency were prioritised, while traditional control principles—such as segregation of duties, independent review, and override mechanisms—were insufficiently applied.

Taken together, these patterns highlight that the effectiveness of AI in finance depends less on technological sophistication and more on the strength of the governance frameworks within which it operates.

Implications for Management Accountants and Finance Professionals

The growing use of AI-driven systems in finance, accounting, and banking does not diminish the role of professional judgment; rather, it fundamentally reshapes it. As AI increasingly influences forecasts, valuations, credit decisions, and risk assessments, management accountants and finance professionals are required to move beyond being users of outputs to becoming critical evaluators of how those outputs are generated and applied.

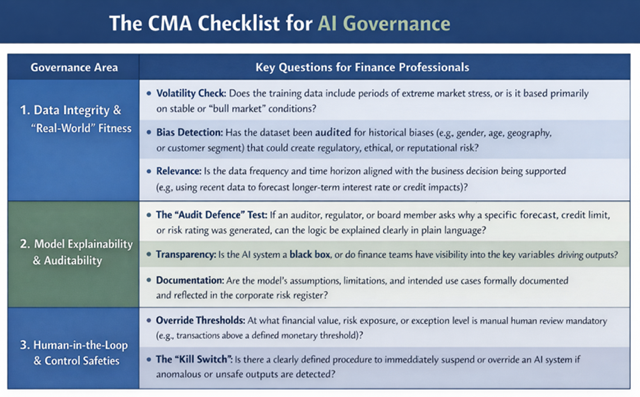

One key implication is the need to apply traditional finance and control disciplines to AI-driven systems. This includes robust validation, stress testing under adverse scenarios, clear documentation of assumptions, and independent review—principles long applied to financial models, but not always extended to advanced analytics and machine-learning tools. AI-driven outputs should be treated as decision-support inputs, not authoritative conclusions.

There is also a heightened responsibility around governance and accountability. Finance professionals are often best placed to define ownership of AI-driven decisions, establish escalation and override mechanisms, and ensure compliance with regulatory, ethical, and organisational standards. Where AI systems lack transparency or explainability, it is incumbent on professionals to challenge their suitability for high-impact decisions.

In an increasingly automated environment, the enduring value of management accountants and finance professionals lies in safeguarding decision quality, integrity, and trust.

Conclusion

The growing presence of AI-driven systems in finance, accounting, and banking represents a significant shift in how decisions are informed and executed. While these technologies offer clear benefits in terms of efficiency, scale, and analytical capability, recent failures demonstrate that AI does not eliminate risk—it redistributes it. In many cases, the most serious consequences arise not from technical shortcomings, but from weaknesses in governance, oversight, and professional challenge.

For management accountants and finance professionals, AI failures serve as a reminder that accountability cannot be automated. Regardless of how sophisticated a system may appear, responsibility for decisions ultimately rests with those who design, approve, and rely on its outputs. Professional judgement, scepticism, and ethical awareness remain essential, particularly where AI-driven insights influence high-impact financial and strategic outcomes.

As organisations continue to embed AI into core processes, the role of finance professionals becomes even more critical. Their value lies not in competing with algorithms, but in ensuring that AI-driven decisions are transparent, controlled, and aligned with sound financial principles. In this sense, AI failures do not diminish the relevance of the profession—they reaffirm it.

AI does not remove judgment from finance; it relocates it, often to places where accountability is least visible.

References

ACLU (2018), “Why Amazon’s automated hiring tool discriminated against women”, American Civil Liberties Union, October 10, https://www.aclu.org/news/womens-rights/why-amazons-automated-hiring-tool-discriminated-against

GeekWire (2021), “iBuying algorithms failed Zillow, says business world’s love affair with AI”, GeekWire, November 4, https://www.geekwire.com/2021/ibuying-algorithms-failed-zillow-says-business-worlds-love-affair-ai/

ACLU (2018), “Why Amazon’s automated hiring tool discriminated against women”, American Civil Liberties Union, October 10, https://www.aclu.org/news/womens-rights/why-amazons-automated-hiring-tool-discriminated-against

Advisory.com (2018), “IBM’s Watson recommended unsafe and inaccurate cancer treatments, report finds”, Advisory Board Daily Briefing, July 27, https://www.advisory.com/daily-briefing/2018/07/27/ibm

Dastin, J. (2018), “Amazon scraps secret AI recruiting tool that showed bias against women”, Reuters, October 10, https://www.reuters.com/article/world/insight-amazon-scraps-secret-ai-recruiting-tool-that-showed-bias-against-women-idUSKCN1MK0AG

Forbes (2021), Taulli, T., “IBM Watson: Why is healthcare AI so tough?”, Forbes, February 27, https://www.forbes.com/sites/tomtaulli/2021/02/27/ibm-watson-why-is-healthcare-ai-so-tough/

Harvard Business School (2019), “Gender bias complaints against Apple Card signal a dark side to fintech”, HBS Working Knowledge, November 18, https://www.library.hbs.edu/working-knowledge/gender-bias-complaints-against-apple-card-signal-a-dark-side-to-fintech

Inside AI News (2021), “The $500m debacle at Zillow Offers: What went wrong with the AI models”, Inside AI News, December 13, https://insideainews.com/2021/12/13/the-500mm-debacle-at-zillow-offers-what-went-wrong-with-the-ai-models/

The Guardian (2019), “Apple Card issuer investigated after claims of sexist credit checks”, The Guardian, November 10, https://www.theguardian.com/technology/2019/nov/10/apple-card-issuer-investigated-after-claims-of-sexist-credit-checks

US Securities and Exchange Commission (2013), “SEC charges Knight Capital with violations of Market Access Rule”, SEC Press Release, October 16, https://www.sec.gov/newsroom/press-releases/2013-222

Wikipedia (2024), “Knight Capital Group”, Wikipedia, https://en.wikipedia.org/wiki/Knight_Capital_Group

Mr. Kapila Dodamgoda, BEng. FCMA, is the ICMA(ANZ) Regional Director for Sri Lanka